The year 2025 will likely be remembered as one of rebalancing and renewal across global markets. Despite deep political divisions, trade disruptions, and uneven recoveries from prior economic shocks, most asset classes — from metals to bonds — delivered strong returns. It was a year that rewarded resilience and long-term strategy rather than speculation. For African economies, it provided both challenges and windows of opportunity, as the continent’s role in global supply chains and investment networks became increasingly visible.

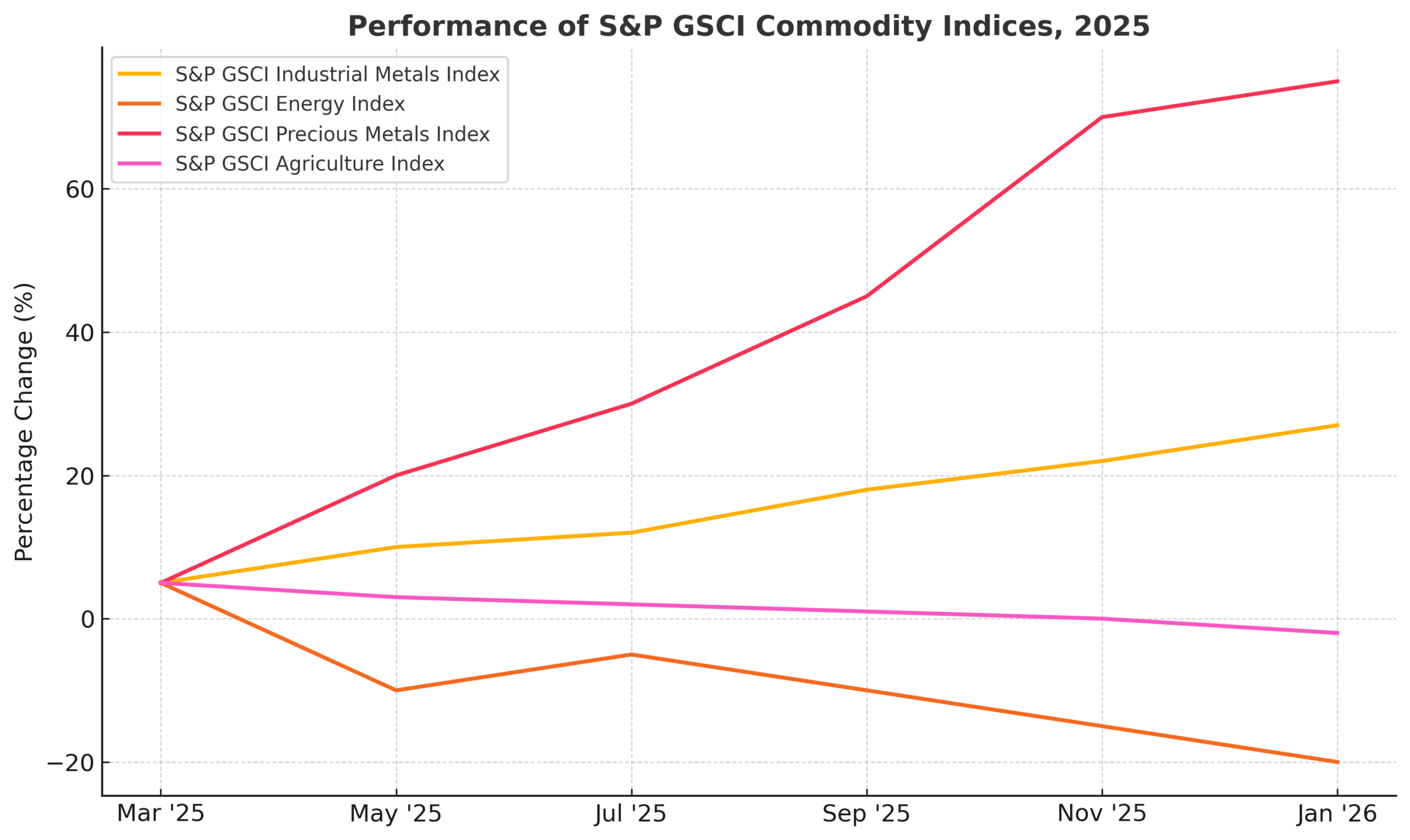

Precious metals were the clear winners of 2025. Silver surged by 148 per cent, its strongest performance in decades, while gold rose 64.6 per cent. The rally reflected silver’s dual identity: both as a safe-haven investment and an essential industrial material powering solar panels, semiconductors, and electric vehicle technologies. The United States’ decision to classify silver as a “critical mineral” under its strategic resource policy further intensified global demand. Meanwhile, constrained supply and low inventories kept markets tight, with African silver and platinum producers benefiting from renewed exploration interest.

Industrial metals also rallied, with copper prices climbing 43 per cent to USD 12,510 per metric tonne on the London Metal Exchange. The boom was fuelled by two key factors: the surge in artificial intelligence (AI) data infrastructure and the rapid scaling of renewable energy projects worldwide. Disruptions in major producing countries such as Chile, Indonesia, and the Democratic Republic of Congo tightened global supply. For Africa, the copper rally revived the strategic importance of the Copperbelt — stretching through Zambia and southern DRC — highlighting the region’s enduring significance to the global energy transition.

Energy markets told a contrasting story. Despite geopolitical tensions, including conflict in Ukraine, trade friction between the United States and Venezuela, and unrest in the Middle East, oil prices declined sharply. Brent and WTI crude fell by roughly 18 and 20 per cent respectively, dragged down by persistent oversupply. OPEC and its allies increased output by nearly three million barrels per day, while American shale producers maintained record production levels. These developments reaffirmed that market fundamentals, rather than geopolitics alone, shaped price movements in 2025.

Agricultural commodities faced headwinds, with wheat and maize declining by 8 and 4 per cent respectively amid abundant harvests. Soybeans rose modestly by 3.6 per cent after a thaw in US–China relations spurred a rebound in Chinese imports. Yet for African economies, where agriculture remains a cornerstone of livelihoods and GDP, 2025 underscored the urgent need for self-sufficiency and regional integration under the African Continental Free Trade Area (AfCFTA). Increasing productivity, reducing post-harvest losses, and improving cross-border logistics will be critical if Africa is to insulate itself from global food price volatility.

Global equity markets notched their third consecutive year of gains, though regional divergence widened. The United States lagged, while Asia, Latin America, and parts of Africa experienced renewed investor optimism. The Johannesburg Stock Exchange and the Nairobi Securities Exchange recorded steady inflows, driven by technology, energy transition, and financial innovation. Across the continent, capital markets continued to mature, with new debt instruments and green bonds gaining traction as vehicles for climate-related investment.

Bonds enjoyed their strongest year since 2020, buoyed by falling interest rates. Central banks in advanced economies reversed much of their earlier monetary tightening, with the Federal Reserve cutting rates three times and the European Central Bank four times. Morningstar’s global bond benchmark rose 7.3 per cent, illustrating renewed confidence in sovereign and investment-grade debt. In contrast, the Bank of Japan bucked the trend, raising rates twice as it sought to normalise decades of unconventional policy. For African debt markets, declining global yields provided breathing room, enabling several countries — including Kenya, Nigeria, and Côte d’Ivoire — to refinance Eurobond maturities under improved conditions.

Corporate performances mirrored these macro shifts. Among the top global gainers were mining group Fresnillo (+436 per cent), buoyed by its exposure to gold and silver; EchoStar (+374 per cent), which recovered after selling valuable licences to SpaceX and AT&T; and Lumentum (+339 per cent), propelled by the explosion in demand for optical components for AI data centres. Bloom Energy (+291 per cent) also stood out, providing clean, continuous power solutions for AI infrastructure. Meanwhile, Micron (+239 per cent) broke industry cyclicality through soaring memory demand, and Robinhood (+203 per cent) doubled its revenues through predictive market innovations. Defence-linked industries such as Renk, Rheinmetall, and Thales also performed well as European governments boosted defence spending in response to shifting geopolitical realities.

Conversely, some high-profile firms faltered. The Trade Desk and Fiserv both tumbled by 67 per cent, hit by declining market share and profit warnings. Lululemon and Chipotle struggled with waning consumer demand, while Diageo suffered a 37 per cent fall as changing health preferences and the spread of anti-obesity medication dented alcohol sales. The most dramatic fall came from UnitedHealth, which lost 35 per cent following regulatory investigations and leadership turmoil.

Despite such corporate volatility, the macroeconomic picture closed on a broadly positive note. Global growth proved resilient, supported by fiscal stimulus and monetary easing. The United States maintained solid expansion, the European Union avoided a downturn, and China achieved its 5 per cent growth target. In Africa, the narrative was one of cautious optimism: Nigeria stabilised its currency through reform, Kenya expanded its technology exports, and South Africa saw renewed mining investment after years of underperformance.

Digital finance and cryptocurrency adoption also continued to grow across the continent. While Bitcoin fluctuated, peaking above USD 125,000 before retreating, African fintech ecosystems — led by Nigeria, Kenya, and South Africa — deepened financial inclusion, proving more adaptive than speculative.

Ultimately, 2025 was not merely a year when global markets “paid off.” It marked a gradual decentralisation of economic power and perspective. Africa’s role — as both a resource hub and an innovation frontier — became harder to ignore. As the global economy moves toward 2026, the continent faces the task of consolidating these gains: to transform its resource wealth into sustainable growth and position itself not as a peripheral actor but as a co-architect of a more equitable global economic order.