South African fund managers have expressed a notably optimistic outlook on domestic equities, driven by expectations of economic strengthening and a favourable inflationary environment. According to the latest South Africa Fund Manager Survey, a remarkable 82% of respondents foresee more buys than sells in the forthcoming year, marking a substantial rise in investor confidence.

The survey indicates that 88% of fund managers would overweight domestic stocks over the next 12 months, while 77% are sanguine about equities over the next three to five years. This optimism is underpinned by a net 82% of respondents—up from 47% in June—anticipating a modest strengthening of the economy within the next year. Furthermore, a similar net of 76% expects inflation to moderate slightly over the same period.

Sectoral preferences among fund managers show a pronounced inclination towards banks, apparel retail, and software, reflecting targeted optimism in these areas. This sectoral confidence is underpinned by a broader belief in the South African economy’s potential, bolstered by recent governmental stability and policy measures.

JP du Plessis, a director at Stonehage Fleming, highlighted the stabilising influence of the Government of National Unity (GNU), an encouraging inflation backdrop, and anticipated interest rate cuts as key factors that could catalyse a boom in the Johannesburg Stock Exchange (JSE). The GNU has already positively impacted the JSE All Share Index, which saw a 4.1% return in June, while the JSE Financial Index surged by 13.2% over the same period.

Despite this rally, many JSE-listed companies continue to trade below their long-term average valuation multiples, suggesting further upside potential. Momentum Investments has also signalled a preference for domestic asset classes over global counterparts for the upcoming year, citing more attractive valuations and the potential for rand strength. Nevertheless, the global diversification of many JSE-listed companies mitigates sensitivity to local economic developments and currency fluctuations.

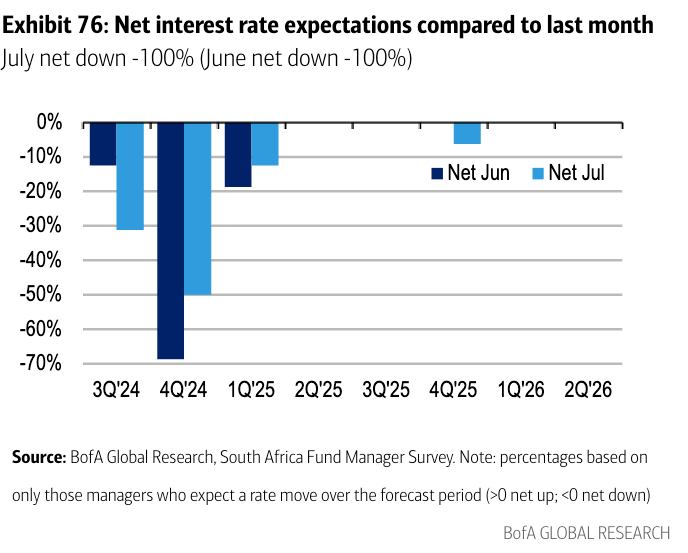

The consensus regarding an interest rate cut has evolved, with Bank of America (BofA)’s fund manager survey revealing a shift towards an earlier reduction. Initially projected for Q4 2024, there is now a growing belief that the first cut may occur in Q3, with 31% of investors—up from 13% in June—holding this view. The survey, conducted between 5th and 11th July, predated the South African Reserve Bank (SARB)’s recent Monetary Policy Committee (MPC) meeting, which resulted in the repo rate remaining at 8.25%. Notably, two of the six MPC members voted for a 25 basis point cut, marking a departure from the previous unanimity on maintaining rates.

BofA’s economists now project a 25 basis point rate cut in September, followed by further reductions in November, January, and March, potentially bringing the repo rate to 7.25%. This represents a significant shift from BofA’s earlier forecast of a January 2025 commencement for rate cuts.

Standard Bank also anticipates the start of the interest rate-cutting cycle in September, with an expected 25 basis point reduction by the MPC.

The burgeoning optimism among South African fund managers, underpinned by expectations of economic fortification and easing inflation, heralds a potentially robust phase for domestic equities. The convergence of favourable government policy, economic indicators, and investor sentiment could pave the way for a significant uptrend in the South African financial markets.